Spain, Denmark and the Netherlands to be the EU hydrogen hot spots – Rabobank.

The momentum for clean hydrogen is growing fast and we’re on the brink of a wave of Financial Investment Decisions. Although, many hydrogen projects have been announced, there’s still a large gap between the total announced capacity and the EC’s ambition for 2030. On a member state level, Spain, Denmark and the Netherlands stand out, all three for very specific reasons. What they have in common, is that they are likely to become the EU’s hydrogen hot spots.

Momentum for Clean Hydrogen Is Growing

Over the past 12 months, the momentum for clean hydrogen[1] in Europe has picked up significantly. There are three main reasons for this acceleration. First, the Russian invasion of Ukraine caused extremely volatile gas prices.

This forced Europe to look for alternatives to Russian gas. It also changed Europe’s perception of energy independence and security. More energy autonomy and greater geographical diversification of energy supplies are top priorities. Clean hydrogen plays a crucial role in achieving this.

🔥 What about we co-host a webinar? Let's educate, captivate, and convert the hydrogen economy!

Hydrogen Central is the global go-to online magazine for the hydrogen economy, we can help you host impactful webinars that become a global reference on your topic and are an evergreen source of leads. Click here to request more details

Second, the US Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) with its ‘simple’ tax credits, gave a boost to clean hydrogen initiatives in the US since their adoption in 2022. EU politicians are growing concerned that this will draw investments away from Europe toward the US. This prompted a swift response from the European Commission (EC). Massive funds have been made available to match or even surpass US support schemes for the development and deployment of renewable energy sources and technologies, including hydrogen.

Third, there’s been an acceleration in EU policymaking. Binding targets have been set for renewable hydrogen. The revised Renewable Energy Directive (RED II) includes a binding target for all EU industry players currently using gray hydrogen.[2] They must replace at least 42% of their gray hydrogen with renewable hydrogen by 2030. One of the largest consumers of gray hydrogen are ammonia producers. Most ammonia is used in the production of fertilizers. Methanol producers are also large consumers of hydrogen.

Methanol is a chemical building block for hundreds of everyday products. Oil refinery, the largest user of hydrogen, is categorized as Transport. This sector is required to include at least 1% hydrogen-based fuels in the fuel mix by 2030. Specific binding targets for the maritime and aviation sectors have been set in the ReFuelEU Aviation and Fuel EU Maritime Directives.

Another important push for renewable hydrogen is REPowerEU. This plan includes specific measures to accelerate the production of renewable hydrogen with the aim of producing 10 megatons (Mt) in Europe and importing 10Mt by 2030. This will require the deployment of 120 gigawatts (GW) of electrolyzer capacity in Europe, powered by 500TWh of new renewable power generation sources.

The total investment associated with these ambitions is expected to be in the range of EUR 335bn to EUR 471bn, of which EUR 200bn to EUR 300bn will be required for additional renewable electricity sources. REPowerEU is backed by a EUR 300bn funding scheme, of which EUR 72bn will be in grants and EUR 225bn in loans.

We’re on the Brink of a Wave of Financial Investment Decisions

More than three years have passed since the first consortia in Europe announced plans to build hydrogen plants. Today, plans for well over a hundred facilities have been announced in Europe. However, almost none of the projects have as yet passed the Final Investment Decision (FID) stage, which is relevant as it marks the actual start of the execution and construction stage. Instead, timelines have been stretched due to many uncertainties such as regulatory issues and terms of subsidy schemes.

Nevertheless, several notorious uncertainties have been resolved in the last 12 months. The definition of renewable hydrogen has finally been agreed upon. Also, dedicated hydrogen subsidy schemes have been made available, such as the European Hydrogen Bank and H2Global.

National subsidy schemes are starting to get allocated. Moreover, the notorious chicken and egg problem has been tackled by setting binding targets for the consumption of renewable hydrogen in the industry and transport sectors, which creates a demand pull and therefore more security for investors.

Yet not all bottlenecks have been solved. The most important constraint is the lack of dedicated infrastructure, such as pipelines, terminals, refueling stations and large-scale ammonia crackers. The choice of hydrogen carrier is also often still a question mark, as pure hydrogen is difficult to handle and transport. Another bottleneck is the availability of vessels for long-distance transportation, preferably with internal combustion engines that run on a hydrogen-based fuel.

This means that projects that will soon reach the FID stage, are likely to be projects where the offtaker is in close proximity of the hydrogen plant. Also projects that will be connected to a soon to be realized hydrogen pipeline can reach a FID if their offtaker will also be connected to that same pipeline.

There’s Still a Giant Gap Between Ambition, Targets and Plans

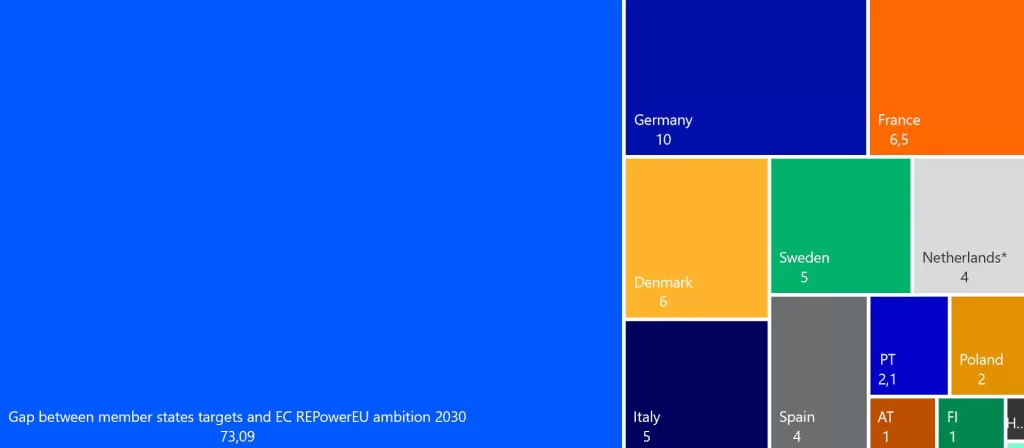

The ambition of 10Mt domestic renewable hydrogen production capacity in the EU, as expressed in the REPowerEU plan, requires an installed electrolyzer capacity of 120GW. Of the EU-27 member states, only 13 have a hydrogen strategy with a specific electrolyzer capacity target. Together they add up to 47GW, not even half of the estimated 120GW needed to realize the EC’s ambition.

The governments of Germany, France and Denmark have the highest ambitions for 2030 (see Figure 1). However, it is fair to mention that the Netherlands’ target of 4GW by 2030 has recently been followed by an 8GW target for 2032.

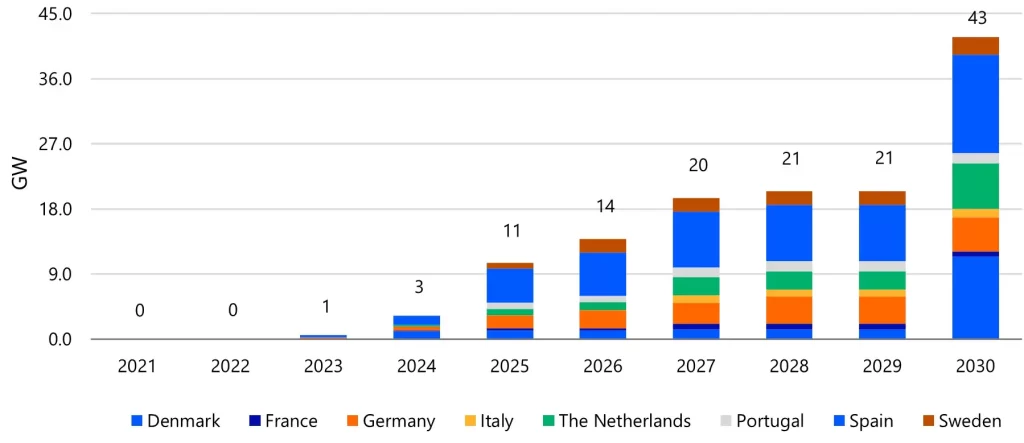

However, government targets do not necessarily translate into private initiatives. When all private plans are added up, the total planned nameplate capacity[3] remains at a mere 43GW in 2030. This falls short of the combined national targets of 47GW, let alone the desired 120GW of electrolyzer capacity needed to realize the EC’s ambition. Realistically, we do not expect this 77GW gap to be bridged by 2030.

Figure 2 shows the cumulative announced electrolyzer capacity per country by planned commissioning year. These numbers come with a high degree of uncertainty. First, because the nameplate capacity in combination with the timelines is not always clearly communicated. Second, some projects are planned in multiple phases, and it is not always clear whether announcements of new phases concern additions or cumulative capacity.

Third, it is highly likely that many projects will experience significant delays or be canceled, given that almost none have reached the FID stage today. Moreover, the fact that the announced nameplate capacity is to almost double between 2029 to 2030 provides little comfort that 43GW will actually be installed by 2030. Perhaps 10GW to 15GW would be a more realistic figure, a far cry from the 120GW the EC envisages.

Spain Emerges as Preferred Location for Green Hydrogen Plants

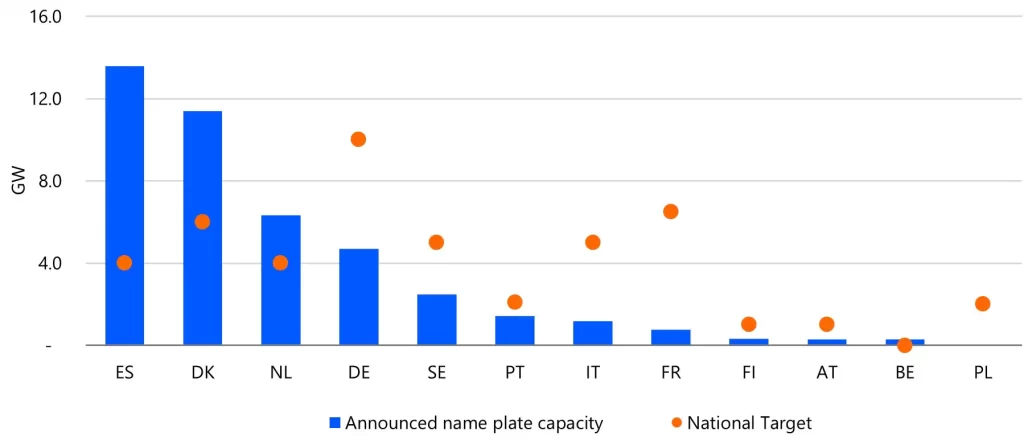

The picture becomes more interesting when we look at the targets of individual member states compared to their announced projects. Figure 3 shows the national targets together with the announced nameplate capacity in 2030.

It is immediately clear that the announced projects in Spain, Denmark and the Netherlands far exceed the national government target. Spain is the absolute preferred location for green hydrogen plants in the EU, with almost 14GW in announced projects, which is more than three times the national target. In Denmark and the Netherlands, the announcements are two and one and a half times the national target, respectively.

Together, these three countries look set to become the main renewable hydrogen producers in Europe, housing over 70% of total EU production capacity by 2030 if all currently announced plans are realized. In the following paragraphs we will explain why Spain, Denmark and the Netherlands are such attractive locations for renewable hydrogen production.

Access To Cheap Renewable Electricity Makes Spain a Hot Spot

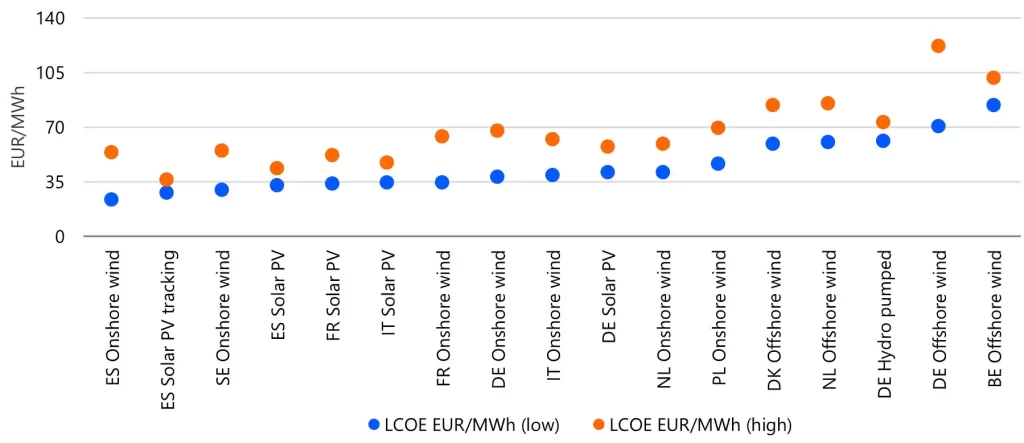

Electricity costs account for 40% to 60% of the cost of renewable hydrogen. The availability of a low-cost renewable electricity source is therefore a precondition for a competitive hydrogen price. The levelized cost of electricity (LCOE) is a measure used to compare the cost of electricity from different energy sources. The LCOE represents the average net present cost of electricity for an electricity source over its lifetime.

A couple of conclusions can be drawn:

- Three out of five of the top five cheapest renewable sources are in Spain.

- In general, solar photovoltaic (PV) systems prevail in southern Europe, and wind in northern Europe.

- The high-low range for solar PV is smaller than for wind, thus indicating better predictability of the energy cost of hydrogen production compared to other renewable energy sources.

Although a low LCOE is important as an input factor for renewable hydrogen production, the capacity factor[4] (also called load factor) also plays an important role in calculating the levelized cost of hydrogen (LCOH). In general, wind has a better capacity factor than solar PV because wind is not limited to daytime as solar PV is.

Much depends on location, of course, but generally speaking, wind can achieve an average capacity factor of 30% to 60%, compared to half that for solar PV. As a consequence, the system CAPEX of the electrolyzer based on wind energy can be amortized over more operating hours, thereby improving the LCOH.

Figure 5 provides examples of modeled LCOH based on the electricity costs from Figure 4 as input in the BloombergNEF Hydrogen Project Valuation Model. We would like to stress that these are LCOH based on an electrolyzer with only a single electricity source and no grid connection.

In practice, an electrolyzer with only a grid connection, or a combination of several electricity sources (wind, solar PV, battery) as well as a grid connection, would make sense for many business cases. It allows the electrolyzer to optimize the number of full load hours, improving the LCOH.

In Figure 5, the lower end of the range represents the modeled LCOH using a western-made alkaline electrolyzer. The upper end of the range represents the modeled LCOH using a more expensive proton exchange membrane (PEM) electrolyzer.[5] The outcomes are illustrative and represent proxy values based on assumptions that are debatable.

Based on Figure 5, a number of observations can be made:

- Spain remains the lowest cost location using onshore wind when the capacity factor is included in the equation.

- Solar PV, despite its low-cost input, becomes less favorable because of its lower capacity factor.

- Dutch and Danish offshore wind are more cost competitive than Spanish fixed axis solar PV.

Figure 5 shows that the capacity factor plays a significant role in the cost of renewable hydrogen and that a cheap renewable electricity source alone is not a sufficient condition for a competitive price of renewable hydrogen. It is also one of the main reasons why Spain is an attractive location for renewable hydrogen plants, especially when onshore wind and solar PV are combined to provide an even better capacity factor.

Another reason is that Spain has a low population density. This leaves sufficient space for the necessary installation of renewable energy sources, together with the hydrogen valleys and hubs located inland. To unlock the production sites, Enagás, the Spanish transmission system operator (TSO), will build a 3,000km hydrogen backbone across Spain.

One of the axes is 1,250km long and runs from the port of Gijon in the north of Spain to the port of Huelva in the south, with a separate connection to Puertollano halfway. The corresponding investments are estimated at EUR 1.85bn.

The other axis is 1,500km long and runs from Gijon in the north to the Mediterranean coast, where it splits into a section running to the port of Cartagena in the south and a section running to the port of Barcelona in the north. The investment associated with this pipeline is EUR 1.65bn.

The Spanish hydrogen backbone will have connections to neighboring Portugal and France. The axis from Barcelona to Marseille in France will be a subsea pipeline called the H2Med project. In December 2022, a memorandum of understanding (MoU) was signed between Enagás, the French TSO GRTGaz and the Portuguese TSO REN to collaborate on the development of this H2Med project, which should be operational by 2030. In January this year, Germany decided to join the project. The total investment for this project is estimated at EUR 2bn to EUR 3bn.

In addition to the hydrogen backbone, maritime hydrogen corridors between Spain and the Netherlands have been agreed upon. For this purpose, several MoUs have been signed this year between Spanish and Dutch parties.

Denmark’s Offshore Wind Potential and Its Proximity to Germany

Denmark’s LCOE for offshore wind is more competitive than its neighbor Germany. Moreover, Denmark has a phenomenal offshore wind potential. Denmark’s national electrolyzer capacity target is 6GW by 2030 and 17GW by 2040. Its offshore wind capacity will grow from 2.3GW today to around 15GW by 2040, complemented by two artificial energy islands with a combined offshore wind capacity of 10GW.

Denmark’s current consumption of gray hydrogen is amongst the lowest in Europe. This will increase in the future as renewable hydrogen is needed to decarbonize the transport sector. However, with Denmark’s ambitious hydrogen and wind plans, the country is poised to become a net exporter of renewable hydrogen before 2030. Based on Denmark’s own national scenarios, exports of renewable hydrogen are expected to increase from 15TWh in 2030 to 79TWh in 2050.

The largest importer of this renewable hydrogen surplus will be its neighbor, Germany. This country is expected to become the largest importer of renewable hydrogen in Europe. According to its updated hydrogen strategy, it will have to import 50% to 70% of its clean hydrogen needs by 2030. This equals 48TWh to 91TWh.

According to the updated hydrogen strategy, Germany’s hydrogen demand will grow to 95TWh to 130TWh by 2030, of which 40TWh to 75TWh should be renewable hydrogen and 55TWh low-carbon hydrogen.

Germany needs large quantities of hydrogen as a back-up for its electricity system. The country will hold auctions for a total of 8.8GW electricity plant capacity between 2023-2028, which should be hydrogen or ammonia-ready. In addition, large quantities of clean hydrogen (renewable and low-carbon hydrogen) are needed to decarbonize its large petrochemical and steel industry. Germany is currently Europe’s largest consumer of gray hydrogen. New uses of hydrogen, such as in the transport sector and in the built environment are also being encouraged.

In March this year, the two neighbors signed an agreement to build a land-based hydrogen pipeline from the border of Jutland in western Denmark, to Schleswig-Holstein in northern Germany. The pipeline is expected to be operational in 2028 and is a collaboration between the TSO Gasunie Deutschland and the Danish TSO Energinet. Additionally, the countries are considering underground hydrogen storage facilities in Lille Torup (Denmark) and Harsefeld (Germany): the SaltHy project developed by Storengy Germany.

Holland Hydrogen Hub

The Dutch target for electrolyzer capacity is 4GW by 2030 and 8GW by 2032. Large hydrogen plants (>100MW) will be located onshore near the landing zones of offshore wind connections and potentially inland at the industrial chemical complex, Chemelot.

The 4GW to 8GW electrolyzer ambition is backed by a target for offshore wind capacity of 21GW in 2030 with a maximum of 70GW in 2050. Like Denmark, the Netherlands benefits from good wind conditions and the shallow waters of the North Sea for its offshore wind electricity production. Not all windfarms can be installed in shallow waters, though. Future plans include deep sea windfarms with electrolyzers on platforms or on artificial islands in the North Sea.

The Netherlands has many underground salt caverns and depleted gas fields where renewable hydrogen can be buffered in large quantities. According to TNO, the technical potential for underground hydrogen storage is estimated at 43TWh in salt caverns and 277TWh in depleted gas fields.[6]

HyStock, a subsidiary of TSO Gasunie, is currently preparing the first salt cavern near Zuidwending for hydrogen storage. The cavern has a storage capacity of 216GWh. Commissioning is planned for 2028. Three more salt caverns will be made suitable for hydrogen storage after 2030.

One of the reasons why the Dutch government is keen on developing local renewable hydrogen production capacity is that the Netherlands is currently the second largest consumer of gray hydrogen in Europe. The Fuel Cells and Hydrogen Observatory estimates that the Netherlands consumes 1.3Mt of gray hydrogen per year compared to 1.7Mt in Germany.

Most of the gray hydrogen is used as a feedstock in the refinery industry, where hydrogen is needed for hydrocracking and hydrotreating processes, including hydrodesulfurization. Other major users of gray hydrogen are currently the chemical industry for the production of ammonia and methanol. In the near future, steel, glass and cement production may also require large quantities of renewable hydrogen, as will the maritime and aviation sectors to decarbonize their activities.

There are five industrial clusters in the Netherlands where heavy industry is located: the port of Rotterdam, the port of Amsterdam, the region of Zeeland, the Chemelot complex in Limburg, and the Groningen seaports. These clusters will be connected in the near future by Gasunie’s hydrogen backbone, which is currently under construction. The hydrogen backbone will largely consist of existing obsolete gas pipelines that will be retrofitted. A connection to Germany and Belgium is also part of the plans.

The first phase will be commissioned in 2025 and will connect the northern and western clusters of the Netherlands. The hydrogen backbone addresses an important bottleneck for renewable hydrogen projects: how to get the hydrogen from the production site to the offtaker.

The Dutch North Sea ports of Rotterdam, Amsterdam and Groningen are building facilities to handle maritime hydrogen imports. Terminals for hydrogen or hydrogen derivatives are being planned in the ports, which will all be connected to the hydrogen backbone. This will allow the ports to transport imported hydrogen to the rest of the Netherlands and export it to Germany and Belgium.

Another corridor, the Delta Rhine Corridor, is planned to run from Rotterdam to Germany. This corridor will likely have six pipelines for the transportation of hydrogen, ammonia, natural gas, LPG, propylene and CO2. Although the Netherlands will not be self-sufficient in renewable hydrogen in the future, it is expected that a substantial share of the imports will be exported to Germany.

Another important future user of low-carbon and renewable hydrogen is the transportation sector. The EC has set a legally binding fuel blending target for the aviation sector starting in 2030. For the maritime sector in Europe, a greenhouse gas reduction scheme has been established, with a first reduction target in 2025.

The ports of Rotterdam, Amsterdam and Schiphol Airport are among the busiest transport hubs in Europe. This means that the Netherlands is likely to see a significant demand for low-carbon and renewable hydrogen-based fuels in the near future.

Spain, Denmark and the Netherlands Are Europe’s Hydrogen Hot Spots

There’s a growing momentum for renewable hydrogen in Europe. Several notorious bottlenecks have been dealt with, paving the way for an expected wave of FIDs on renewable hydrogen production plants in the near future. While this in itself is an appealing prospect, the fact remains that the announced plans fall short of the sum of national targets across the EU-27, which in turn falls short of the total capacity of the EC’s REPowerEU ambition to produce 10Mt of renewable hydrogen domestically per year by 2030.

On an individual member state level, three countries stand out in a positive way. The planned initiatives for renewable hydrogen production capacity in Spain, Denmark and the Netherlands overshoot their own national targets. The three countries excel in renewable hydrogen for different reasons. What they have in common, however, is that new initiatives are likely to gravitate toward these countries, making them the hot spots of the European renewable hydrogen economy.

Highlights:

- Momentum for clean hydrogen is growing fast and we’re on the brink of a wave of Financial Investment Decisions

- We do not expect that the 77GW gap between the EC’s ambition and the announced projects will be bridged by 2030

- Spain, Denmark and the Netherlands stand out in terms of planned electrolyzer capacity because of their specific drivers, which vary greatly from country to country

- These three countries are likely to become the EU’s hydrogen hot spots

Spain, Denmark and the Netherlands To Be The EU Hydrogen Hot Spots, August 31, 2023